April 28th, 2025

5 min. read

By David Collingwood, Director of Workers' Compensation Claims & Safety

Understanding Workers' Compensation Experience Mod Factor

Workers' compensation insurance helps cover medical costs and lost wages for employees who get injured or become ill due to their job. The cost of this insurance can vary based on a factor known as the Experience Modification Factor (or "Experience Mod" for short). Here's a high-level, layman's explanation of the key factors that go into calculating this number, including the policy years considered, and some practical examples.

What is an Experience Mod Factor?

The Experience Mod Factor is a number used by insurance companies to gauge how risky it is to insure a particular employer. A higher number means higher risk, while a lower number suggests lower risk. This factor directly affects how much an employer pays for workers' compensation insurance.

The Experience Mod Factor is calculated by state rating bureaus or the National Council on Compensation Insurance (NCCI) for employers operating in multiple states. These organizations gather claims data reported by insurers and use it to determine each employer's risk profile.

Key Factors in the Calculation:

- Company Size: Larger companies generally have more claims due to having more employees, but this doesn't always mean they're riskier. The Experience Mod takes into account the size of the company by comparing similar-sized companies.

- Claims History: The number and severity of past workers' compensation claims are major factors. Companies with more frequent or severe claims will see higher Experience Mod Factors.

- Industry Risk: Different industries have different levels of risk. For example, construction companies generally have higher risks than office-based businesses. The Experience Mod reflects these industry differences.

- Policy Years Included: The calculation includes the last three completed policy years, excluding the current and most recently completed policy year. For example, if the current policy year is 2024, the Experience Mod calculation will use data from 2020, 2021, and 2022. You may ask why not 2023? Some workers’ compensation claims, depending on severity, can take time to develop before knowing their true exposure. Excluding the most recently completed policy year in the calculation allows a truer picture of the value of those losses when that policy year hits the calculation in the subsequent year.

Rating bureaus recalculate the Experience Mod Factor annually, approximately 90 days before the policy renewal date. This ensures that the most up-to-date claims data is used. - Expected Losses vs. Actual Losses: The Experience Mod compares the company's actual losses to the expected losses. If a company has fewer or less severe claims than expected, its Experience Mod goes down. Conversely, if claims are higher or more severe, the Experience Mod goes up.

Expected Losses: These are the losses that a similar company in the same industry and size would typically have. Insurance companies use historical data to determine these expected losses.

Actual Losses: These are the actual claims that the company has experienced. - Split Rating Approach: The split rating approach differentiates between claim frequency (how often claims occur) and claim severity (how severe the claims are). This approach is used to prevent a few large claims from disproportionately affecting the Experience Mod.

Example: A company experiences several small medical only claims (e.g., minor cuts requiring stitches). These frequent, low-cost claims will have a different impact on the Experience Mod compared to fewer but larger lost time claims (e.g., a severe back injury requiring weeks off work).

Company A has 10 small claims totaling $10,000.

Company B has 1 large claim totaling $10,000.

Under the split rating approach, Company A's frequent small claims might have a less significant impact on their Experience Mod than Company B's single large claim, because the approach aims to reflect both the frequency and severity in a balanced way.

How Expected Losses Are Determined:

Expected losses are calculated based on a combination of industry data and the specific characteristics of the company. Here's a simplified explanation:

- Industry Classification: Every company is classified into an industry group based on the type of work they do. This classification helps insurers compare the company to similar businesses.

- Historical Data: Insurers use historical data from the industry to determine average loss rates. This data includes information about the frequency and severity of claims in similar businesses.

- Payroll Information: The company's payroll is used to help scale the expected losses. Higher payrolls typically correlate with a higher number of employees and, consequently, a higher potential for claims.

- Expected Loss Rate: An expected loss rate is calculated by combining the industry data with the company's payroll. This rate indicates the average amount of losses that a company of this type and size is expected to incur.

Two Claim Types and Their Impact on the Mod:

- Lost Time Claims: A lost time claim occurs when an employee is unable to work due to their injury or illness. For example, an employee suffers a severe back injury and is unable to work for several weeks, resulting in a claim for lost wages and medical costs. Lost Time claims are reported to the Rating Bureaus at 100% of their actual value.

- Medical Only Claims: A medical only claim involves injuries that require medical treatment but do not result in lost work time. For example, an employee cuts their hand and needs stitches but can return to work the next day. This claim only covers the medical expenses. True Medical Only claims are reported to the Rating Bureaus at a 70% Discount of their actual value.

Why the Mod Matters:

- Cost of Insurance: A lower Experience Mod Factor generally means lower insurance premiums, saving the company money.

- Safety Incentives: It encourages companies to improve workplace safety, as a safer workplace can lead to fewer claims and a lower Experience Mod.

By understanding these factors, employers can better manage their workers' compensation costs and create a safer work environment for their employees.

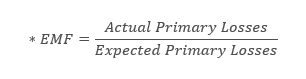

Understanding the Experience Mod Formula and Premium Calculation

The Experience Modification Factor (EMF) is calculated using a formula that compares a company's actual losses to expected losses for similar companies in the same industry. In its simplest terms*, the formula can be expressed as follows:

- Actual Primary Losses: The total amount paid for all primary losses (direct claim costs) during the experience period.

- Expected Primary Losses: The expected amount of primary losses based on industry standards and the company's payroll.

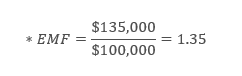

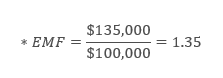

Example Calculation:

- Let's say a company has actual primary losses of $135,000 and the expected primary losses for a similar company in the same industry are $100,000.

In this example, the company's Experience Mod Factor would be 1.35, indicating that their losses are 35% higher than expected. Let’s assume a base premium amount of $50,000. Applying the Mod, actual premium would be calculated at $67,500 ($50,000 x 1.35 = $67,500). - Let’s say the same company has actual primary losses of $82,000 and the expected primary losses for a similar company in the same industry are $100,000.

In this example, the company’s Experience Mod Factor would be 0.82, indicating that their losses are 18% lower than expected. Assuming the same base premium of $50,000, actual premium would be $41,000 ($50,000 x 0.82 = $41,000).

*Formula simplified for demonstration purposes.

Innovative Safety Resources to Reduce Losses

To help drive down losses and, in turn, lower the Experience Mod, companies can implement various innovative safety resources:

- Wearable Safety Devices: These devices monitor workers' health and environment in real-time, alerting them to potential hazards.

- Virtual Reality Training: VR training can increase knowledge retention by simulating real-world scenarios and providing hands-on practice without the associated risks.

- Safety Management Software: This software helps track and manage safety protocols, ensuring compliance and identifying areas for improvement.

- Automated Safety Systems: Automation can reduce human error and exposure to hazardous conditions by taking over dangerous tasks.

- 24/7 Safety Monitoring: Continuous monitoring can detect and address safety issues promptly, preventing accidents before they happen.

- Mental Health Initiatives: Supporting mental health can reduce stress-related injuries and improve overall employee well-being.

By leveraging these innovative resources, companies can create a safer work environment, reduce the frequency and severity of claims, and ultimately lower their Experience Mod Factor.

{kind=link}